Yearly subscription.

Knight-Satchell-Tran’s Moving Average Crossover Model, 1995

$1,200.00

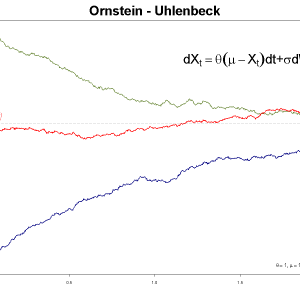

The paper describes a model for (daily) financial asset returns. The model assumes a two state Markov chain: UP (positive returns; up trend) and DOWN (negative returns; down trend). Imposed on each state is a separate Gamma distribution of returns.

The model parameters essentially measure

- the persistence of a trend

- the average size of returns

This advantages of this regime switching model are:

- asymmetric positive and negative returns

- heavy tails

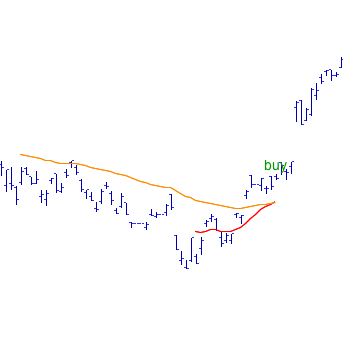

Assuming this particular model, we can compute the expected P&L (and other statistics) of playing two moving average crossover (trend following) strategies:

- GMA(2, 1)

- GMA(∞, 1)

It turns out that for GMA(2, 1) to make money, say off UP trend, the up trend needs to be persistent enough or the average size needs to be big enough. There are exact formulas to quantify these two conditions.

Surprisingly, GMA(∞, 1) is expected to lose money always.

One qualitative conclusion to make is: for a linear trading rule (in prices or returns), such as moving average crossover, we in general prefer to use a small amount of data points rather than all available information.

Reviews

There are no reviews yet.